This project was part of a statistics course in environmental econometrics. My task was to develop a robust model to predict trends in environmental data, as well as write a paper that critically analyses the findings and offers potential contributing factors.

── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

✖ dplyr::filter() masks stats::filter()

✖ dplyr::lag() masks stats::lag()

ℹ Use the conflicted package (<http://conflicted.r-lib.org/>) to force all conflicts to become errors

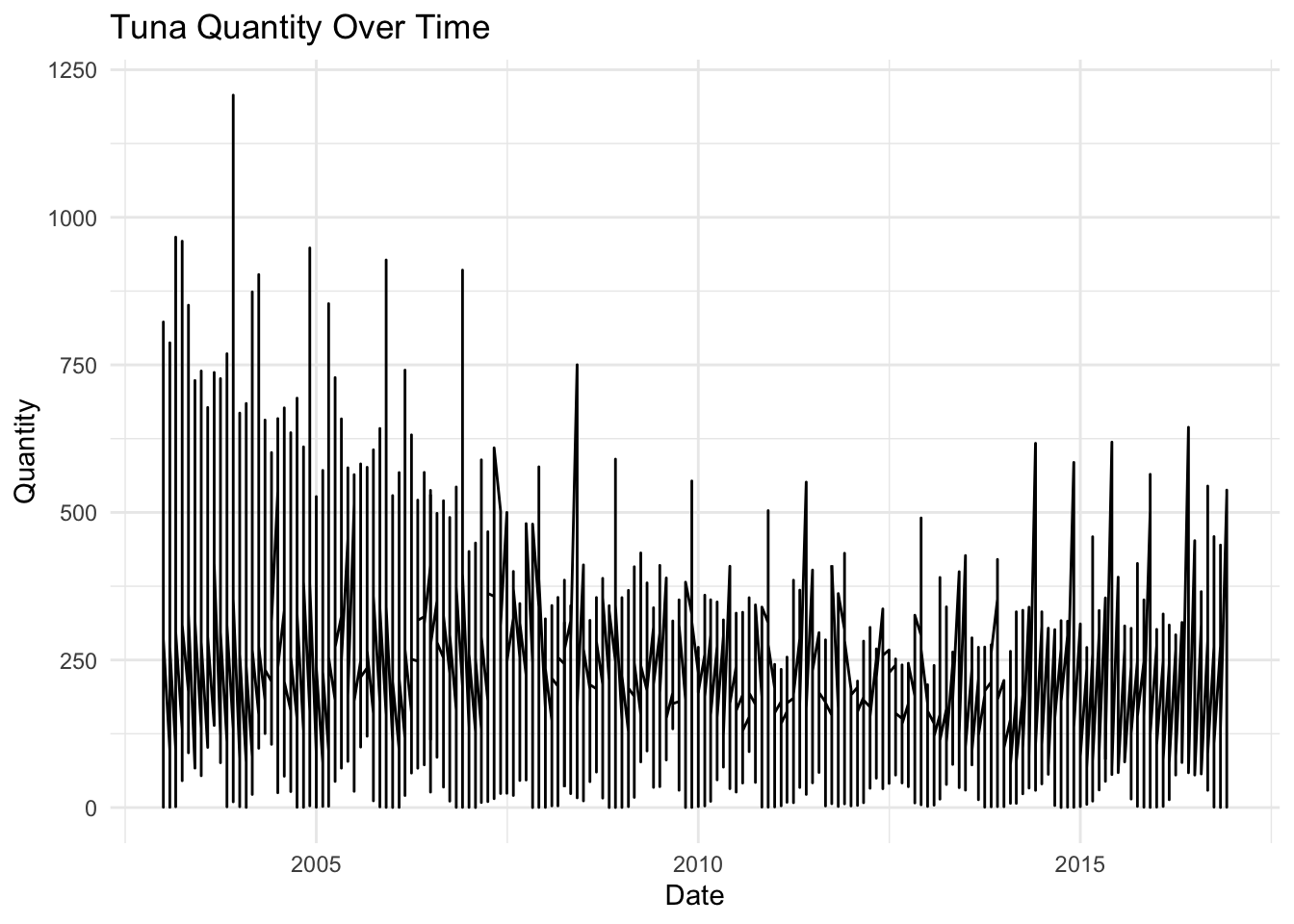

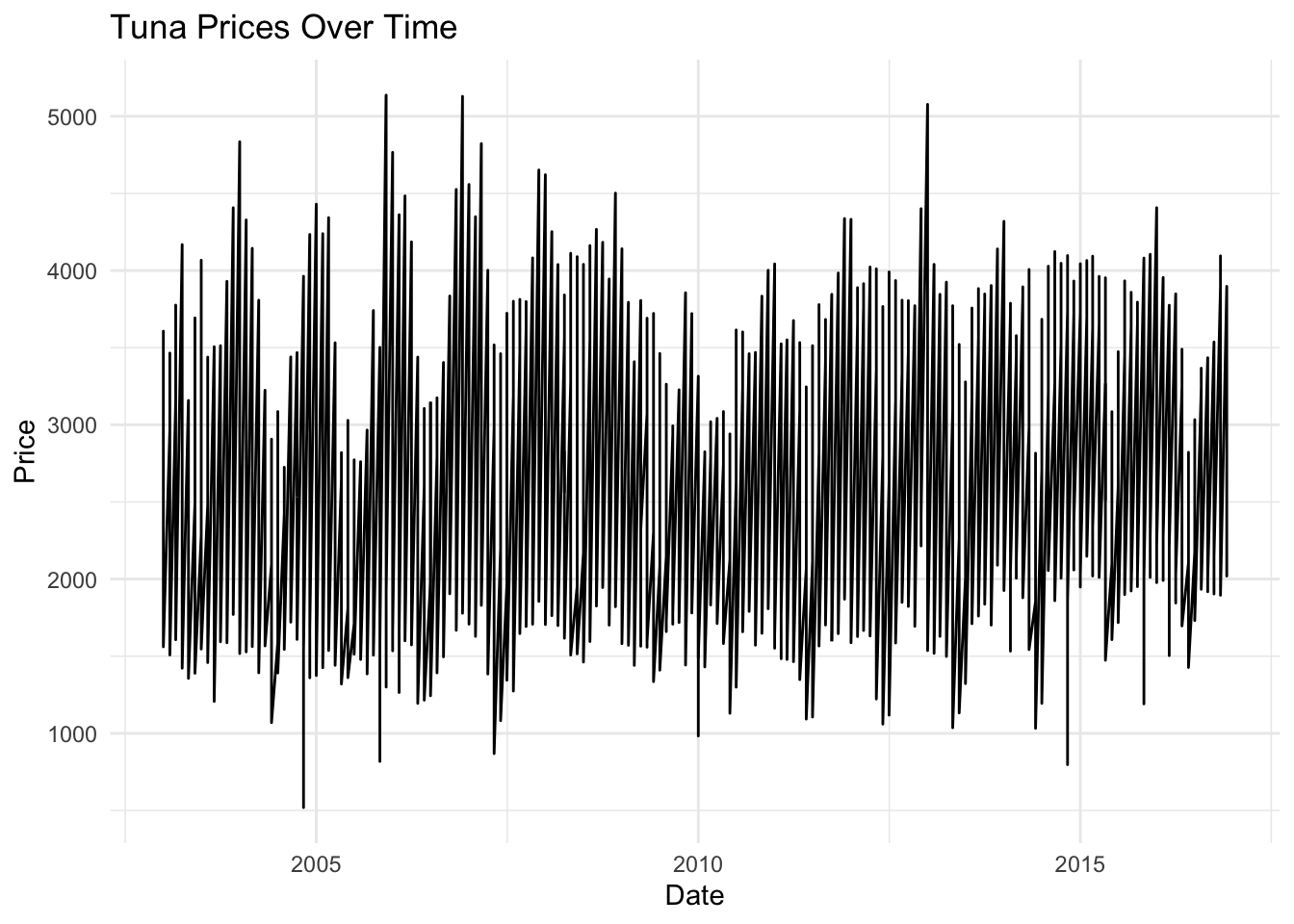

2. Plot Quantity and Price

tuna<-read.csv("/Users/owencallahan/Desktop/R/tokyo_wholesale_tuna_prices.csv")# Combine month and year collumntuna <- tuna %>%mutate(date =make_date(year, month))# Sort data by datetuna <- tuna %>%arrange(date)# Plot Quantitytuna_quantity <- tuna %>%filter(measure =="Quantity")ggplot(tuna_quantity, aes(x = date, y = value)) +geom_line() +labs(title ="Tuna Quantity Over Time", x ="Date", y ="Quantity") +theme_minimal()

# Plot Pricetuna_price <- tuna %>%filter(measure =="Price")ggplot(tuna_price, aes(x = date, y = value)) +geom_line() +labs(title ="Tuna Prices Over Time", x ="Date", y ="Price") +theme_minimal()

3. Model Selection

Trend: Look for any long-term movements or patterns in the data.

Seasonality: Check for repeating patterns at fixed intervals

Randomness: Assess if there are irregular fluctuations or noise.

Decomposition: helps in separating a time series into its components:

When to Use:

If there is a clear trend and/or seasonal pattern in the data, decomposition can help isolate these components for better analysis and forecasting.

Moving Average Smoothing: is used to reduce short-term fluctuations in the data:

When to Use:

To smooth out irregular fluctuations or noise in the data, making underlying patterns more apparent.

Exponential Smoothing: assigns exponentially decreasing weights to older observations:

When to Use:

When the data has no clear trend or seasonality but exhibits random fluctuations.

For short-term forecasting where recent data points are more relevant.

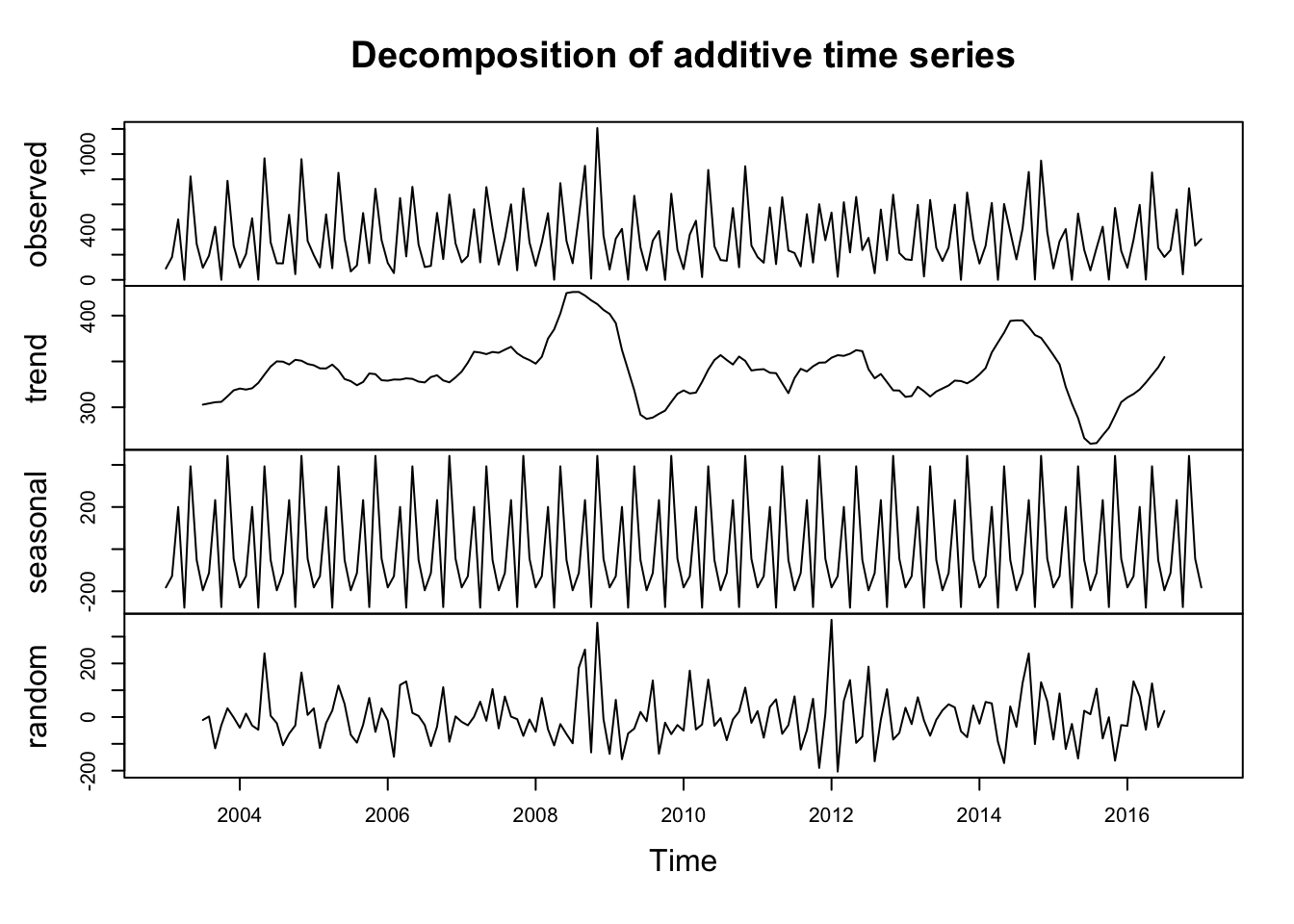

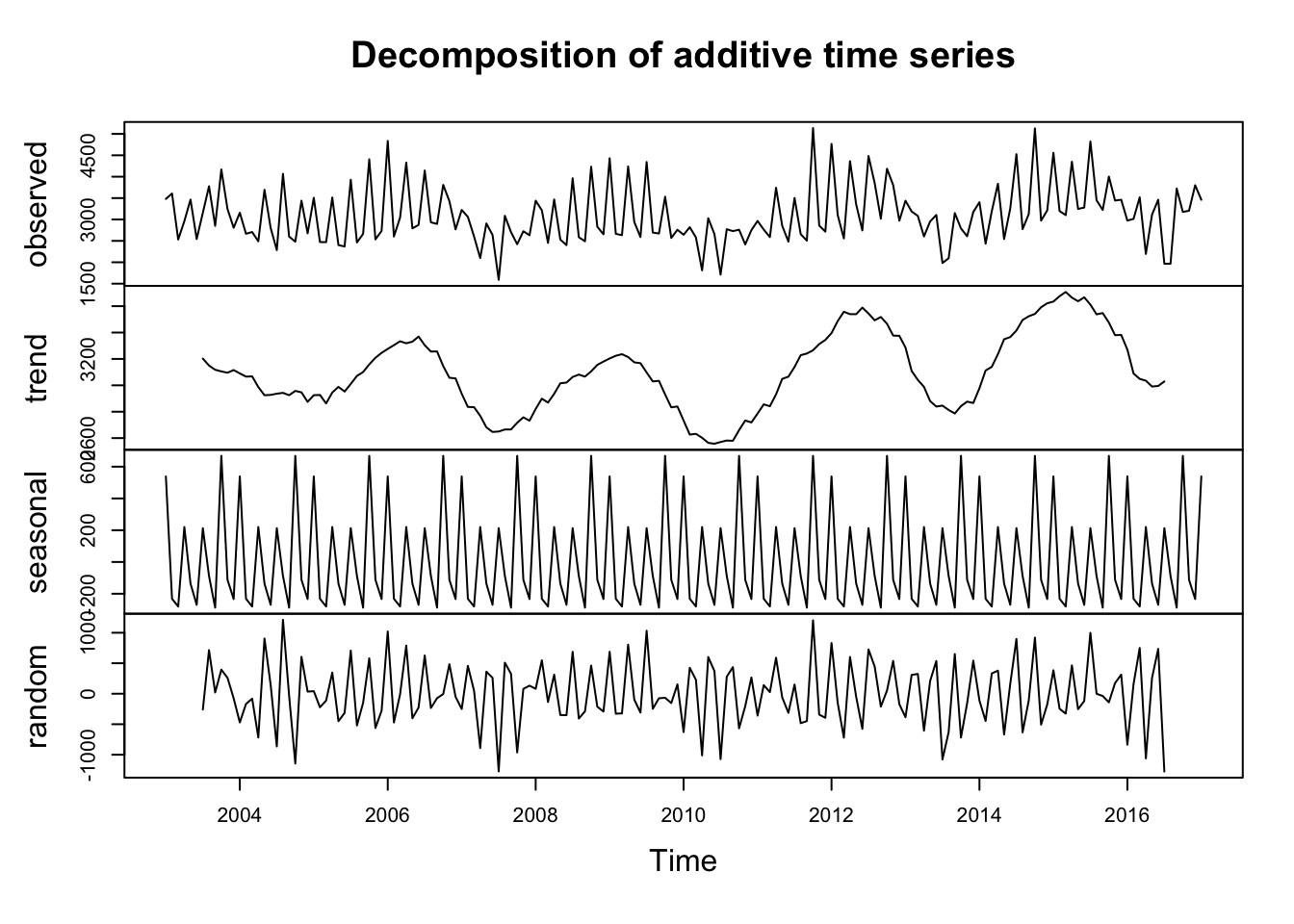

# Quantityts_quan <-ts(tuna_quantity$value, start =2003, end =2017,frequency =12) decomposed1 <-decompose(ts_quan)plot(decomposed1)

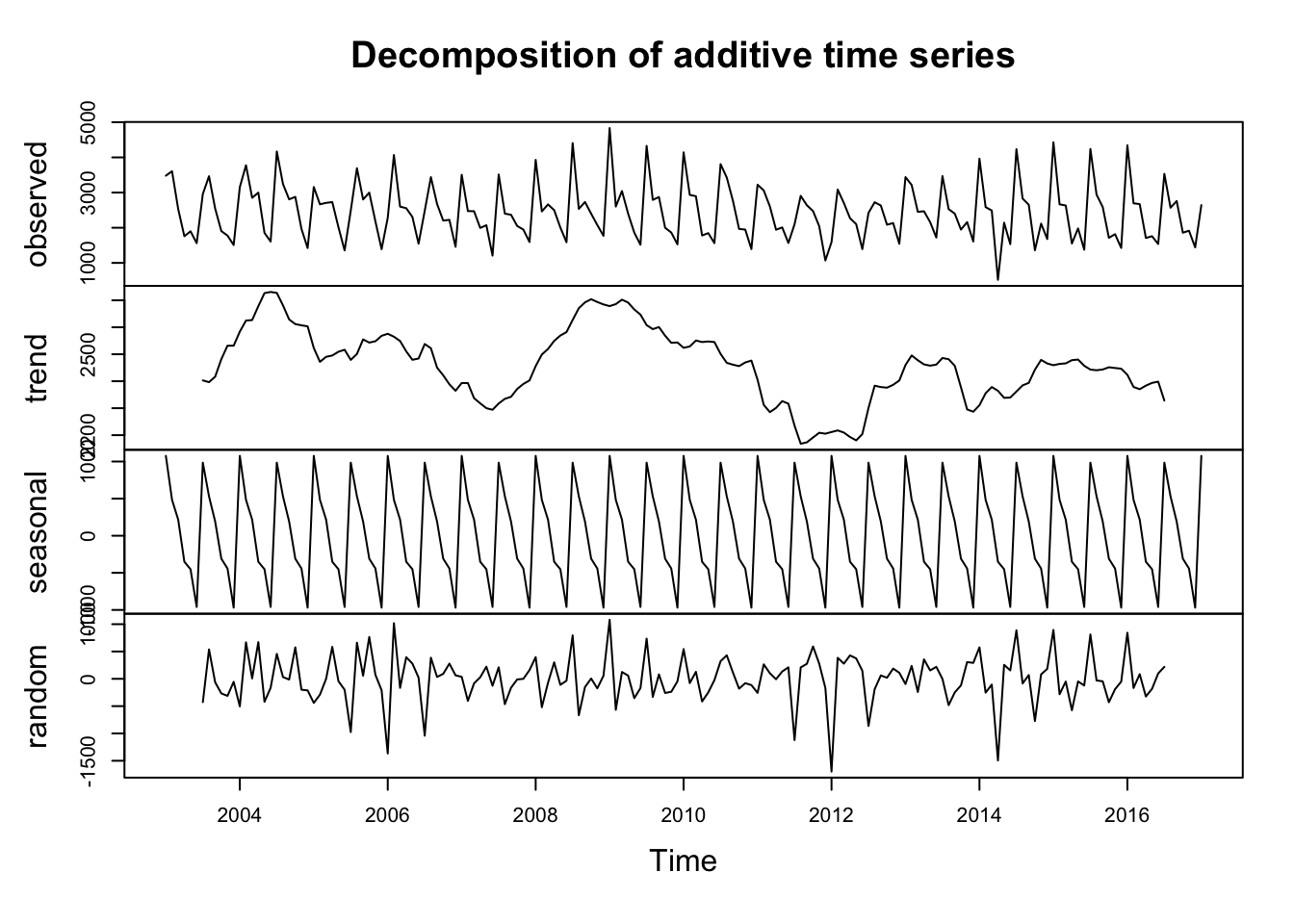

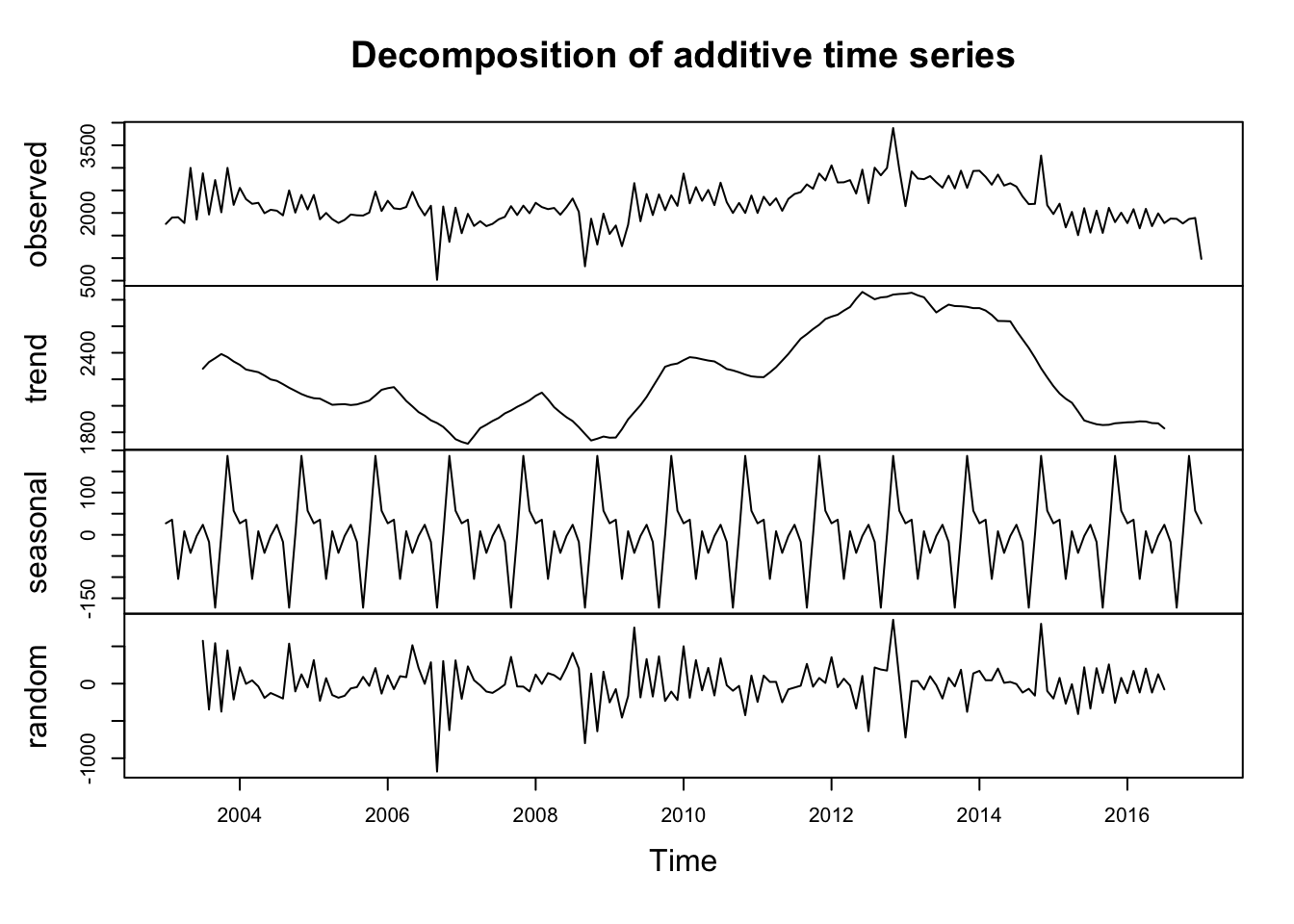

# Pricets_price <-ts(tuna_price$value, start =2003, end =2017, frequency =12) decomposed2 <-decompose(ts_price)plot(decomposed2)

Key Takeaways

Seasonal Component: Appears consistent, suggesting recurring patterns at regular intervals.

Trend Component: Appears less predictable, indicating potential long-term shifts or fluctuations that are not easily captured by a simple pattern.

Random Component: Shows variability, indicating unexplained fluctuations or noise in the data.

4. Test for Stationarity

The ADF test is a statistical test that assesses whether a time series is stationary. Stationarity means that the statistical properties of a time series (such as mean, variance, and autocorrelation) do not change over time.

A more negative ADF statistic indicates stronger evidence for stationarity.

Augmented Dickey-Fuller Test

data: ts_price

Dickey-Fuller = -2.7664, Lag order = 5, p-value = 0.2563

alternative hypothesis: stationary

adf_test <-adf.test(ts_quan)print(adf_test)

Augmented Dickey-Fuller Test

data: ts_quan

Dickey-Fuller = -3.0099, Lag order = 5, p-value = 0.1547

alternative hypothesis: stationary

Key Takeaways

Price model is not stationary

Quantity model is not stationary

5. Fit an ARIMA model

# Fit modelfit_price <-auto.arima(ts_price)fit_quan <-auto.arima(ts_quan)# Summarysummary(fit_price)

Series: ts_price

ARIMA(0,0,0)(0,1,1)[12] with drift

Coefficients:

sma1 drift

-0.8494 -1.3377

s.e. 0.0865 0.8690

sigma^2 = 235806: log likelihood = -1200.48

AIC=2406.96 AICc=2407.12 BIC=2416.13

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 12.06902 465.0506 303.0941 -3.201486 13.59532 0.840122 -0.05292377

summary(fit_quan)

Series: ts_quan

ARIMA(0,0,0)(1,1,0)[12] with drift

Coefficients:

sar1 drift

-0.4004 0.1308

s.e. 0.0729 0.6294

sigma^2 = 16957: log likelihood = -987.28

AIC=1980.57 AICc=1980.72 BIC=1989.73

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set 0.9639297 124.7093 87.62616 -578.987 607.8686 0.9004508

ACF1

Training set -0.01891516

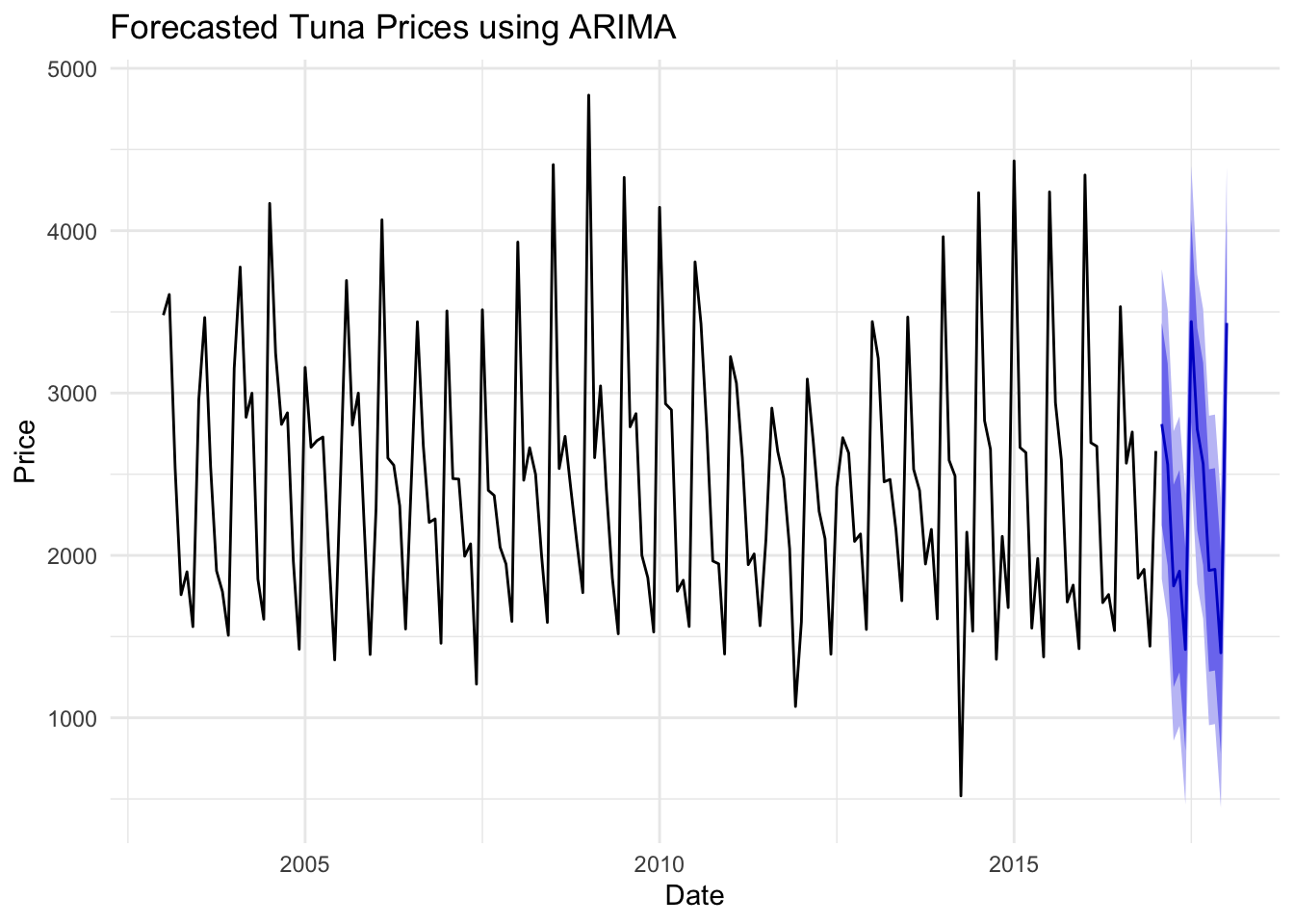

# Forecasting Pricefore_price <-forecast(fit_price, h =12)autoplot(fore_price) +labs(title ="Forecasted Tuna Prices using ARIMA", x ="Date", y ="Price") +theme_minimal()

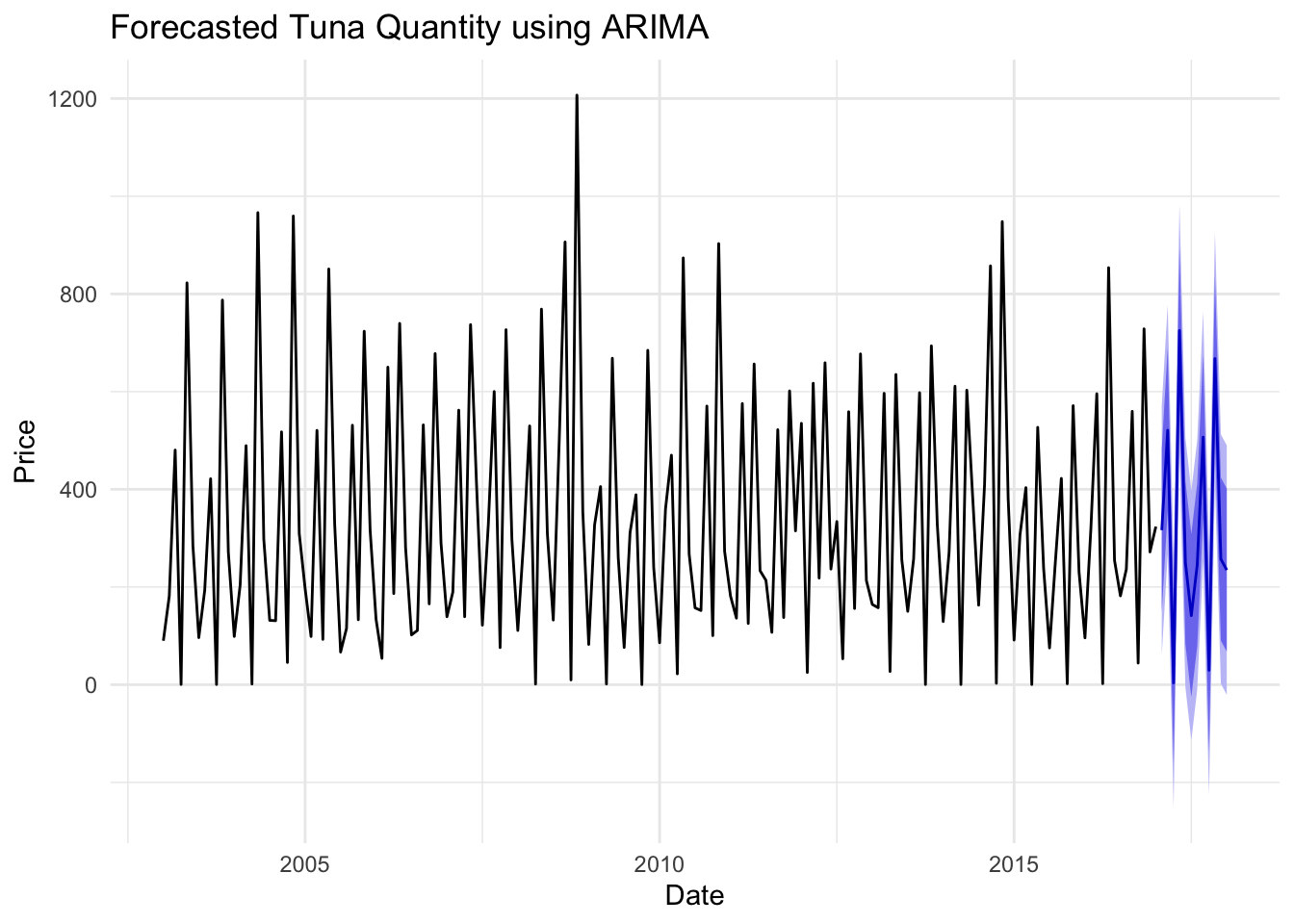

# Forecasting Quantityfore_quan <-forecast(fit_quan, h =12) autoplot(fore_quan) +labs(title ="Forecasted Tuna Quantity using ARIMA", x ="Date", y ="Price") +theme_minimal()

6. Evaluate Results

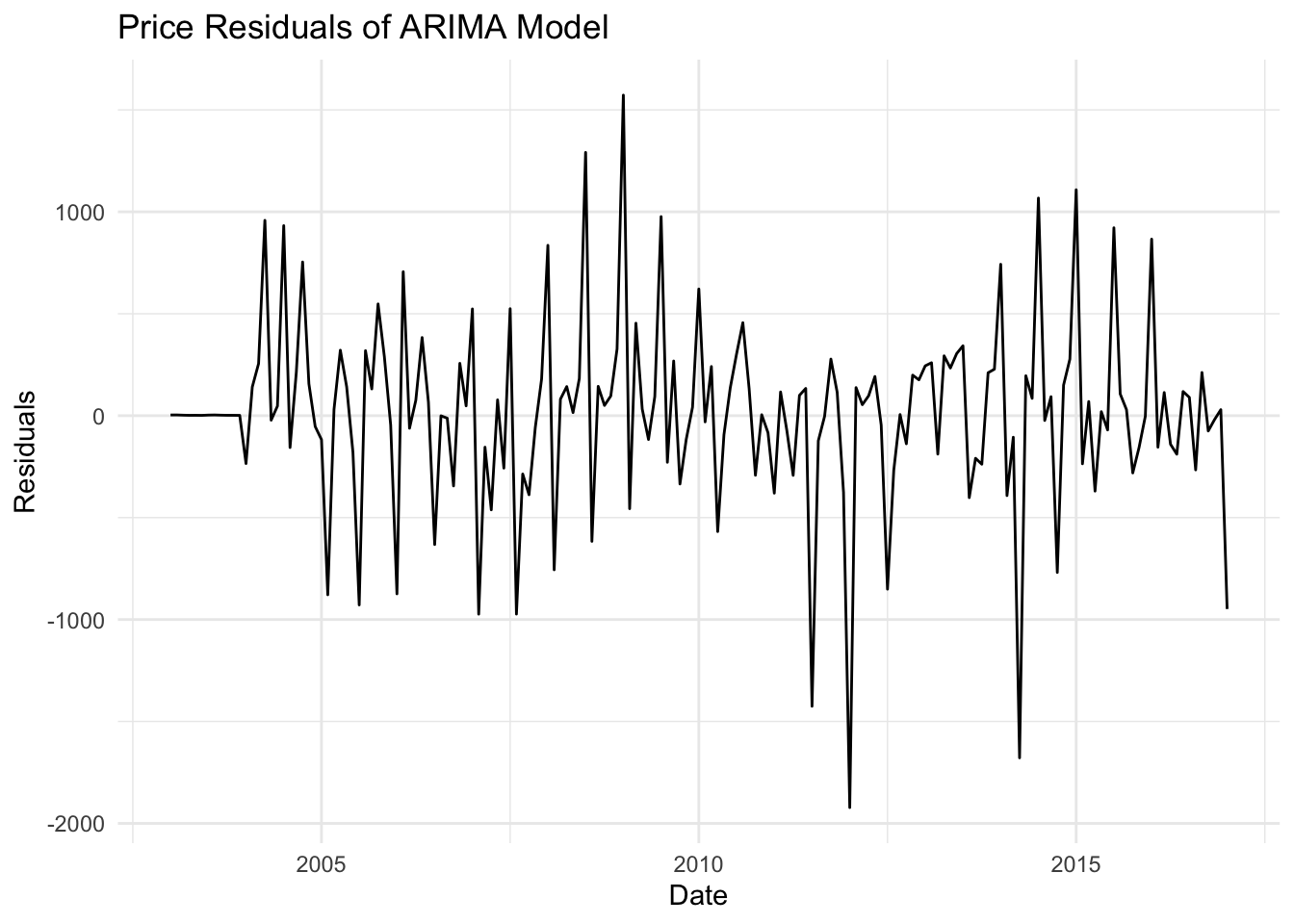

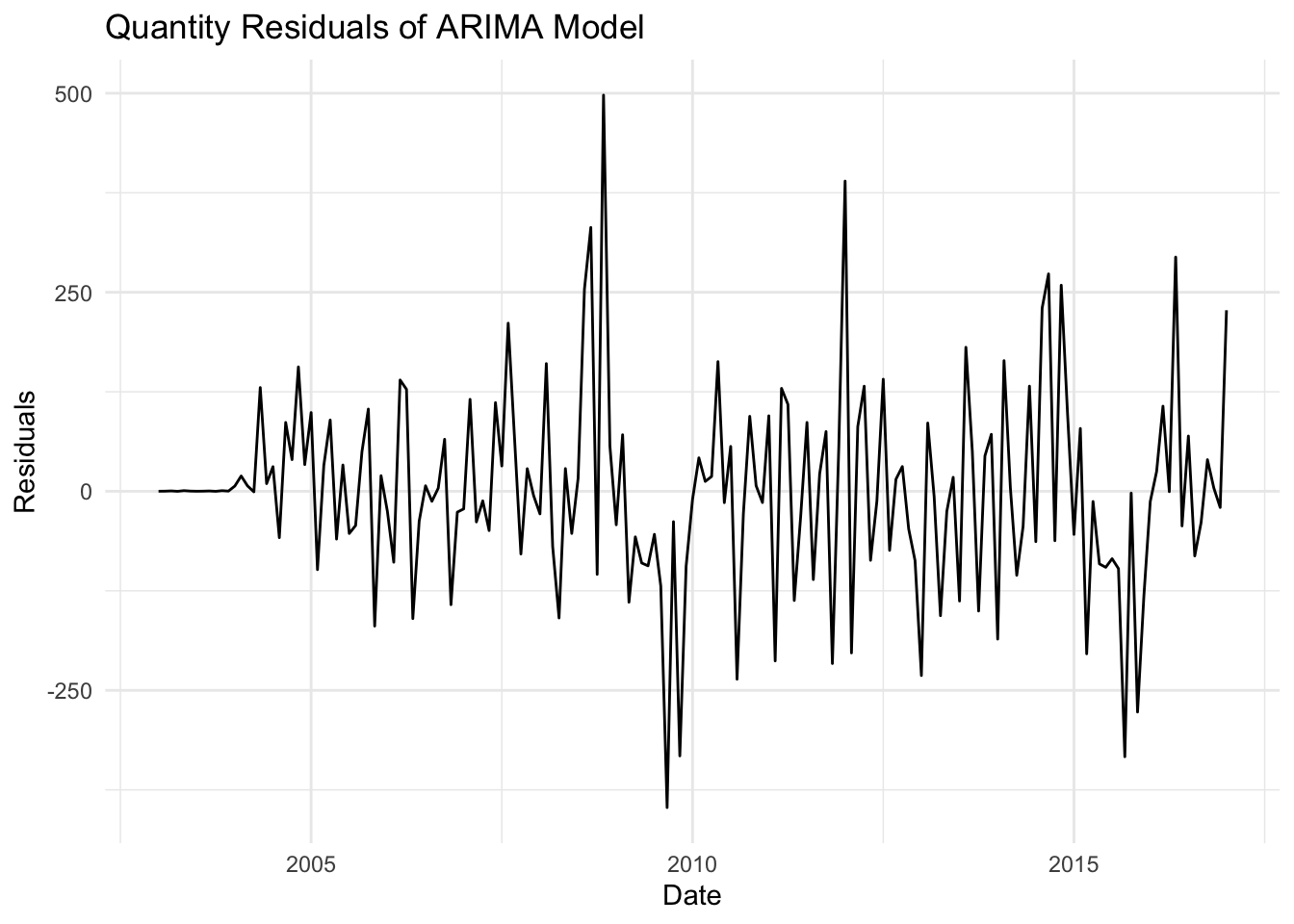

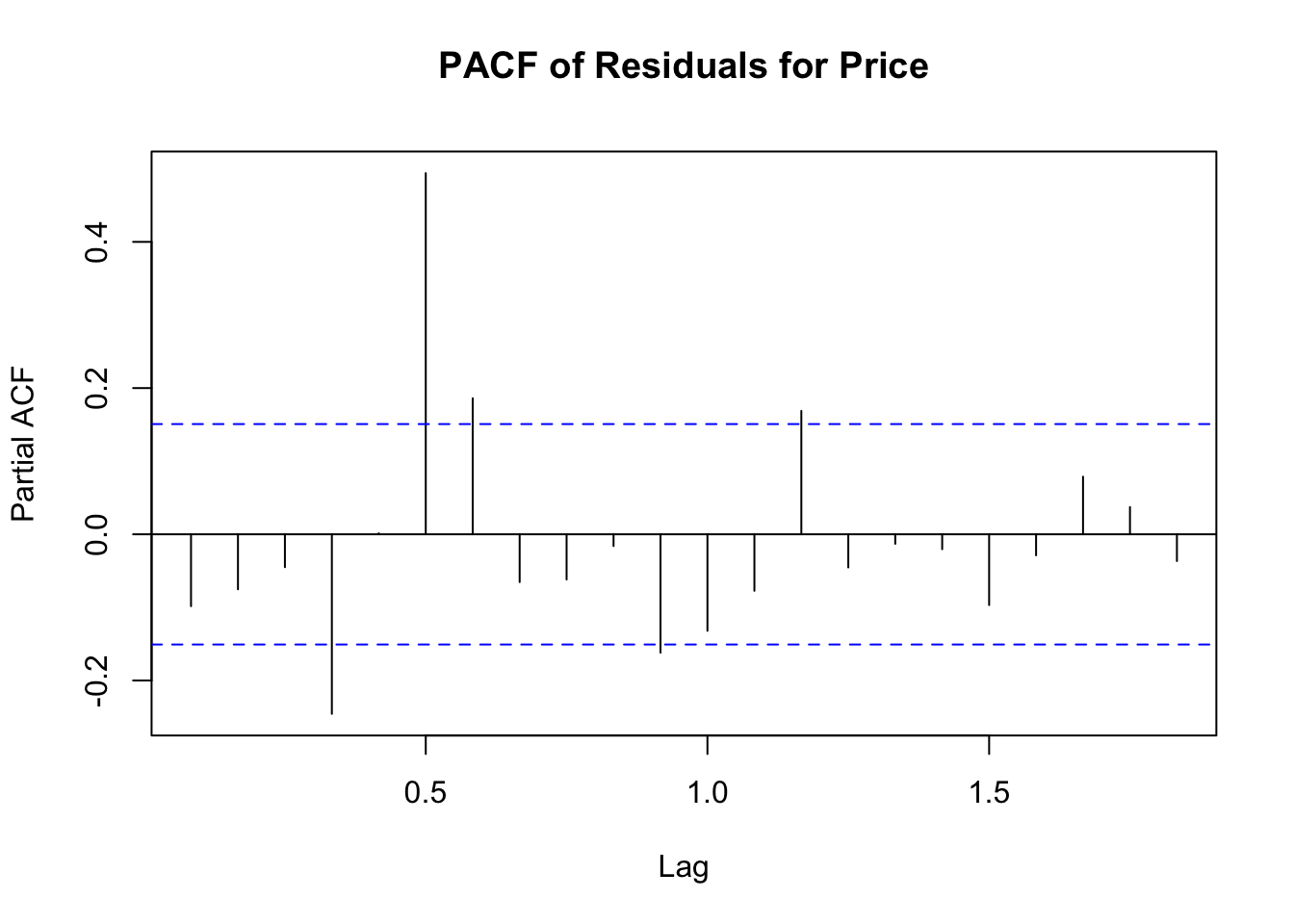

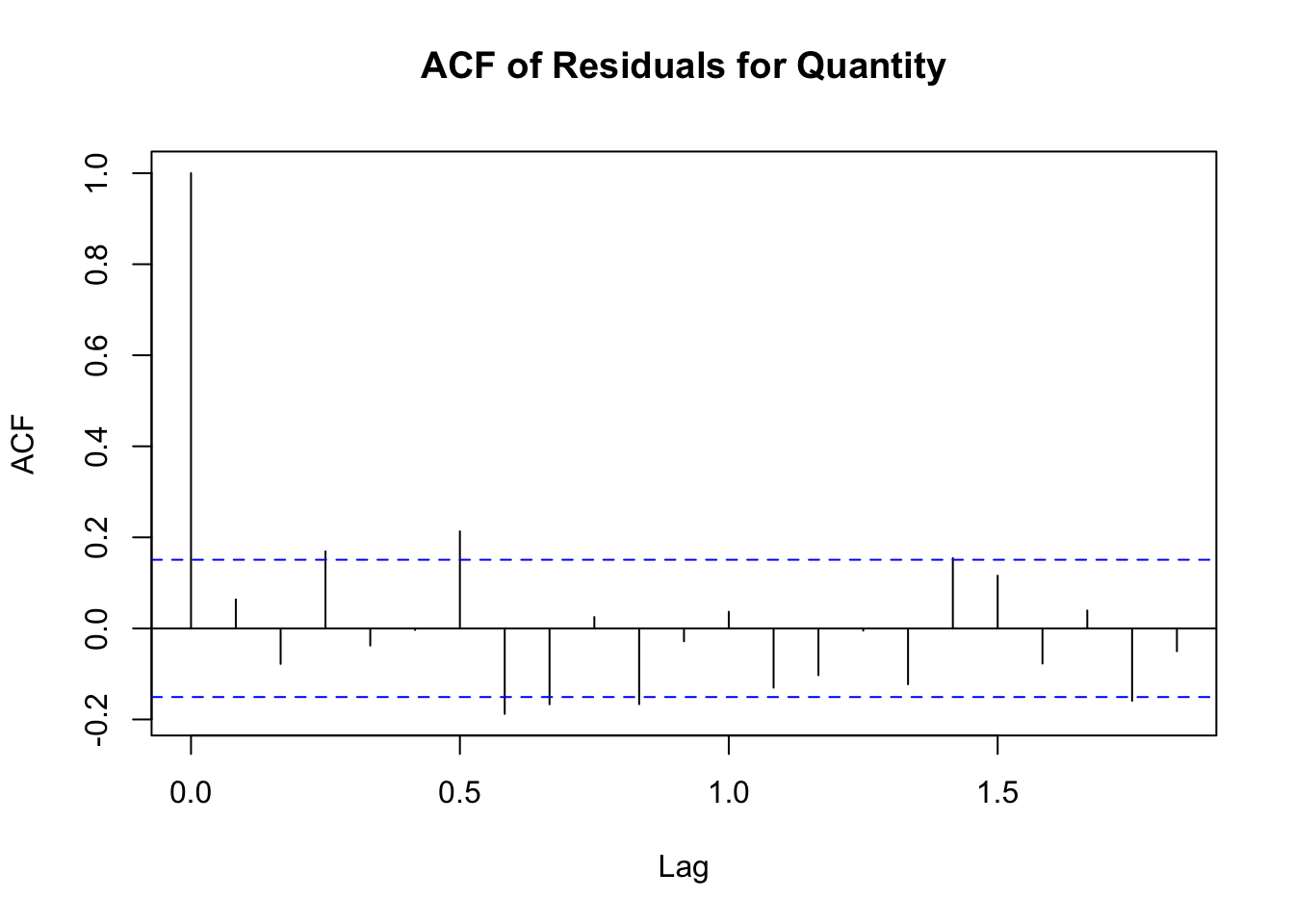

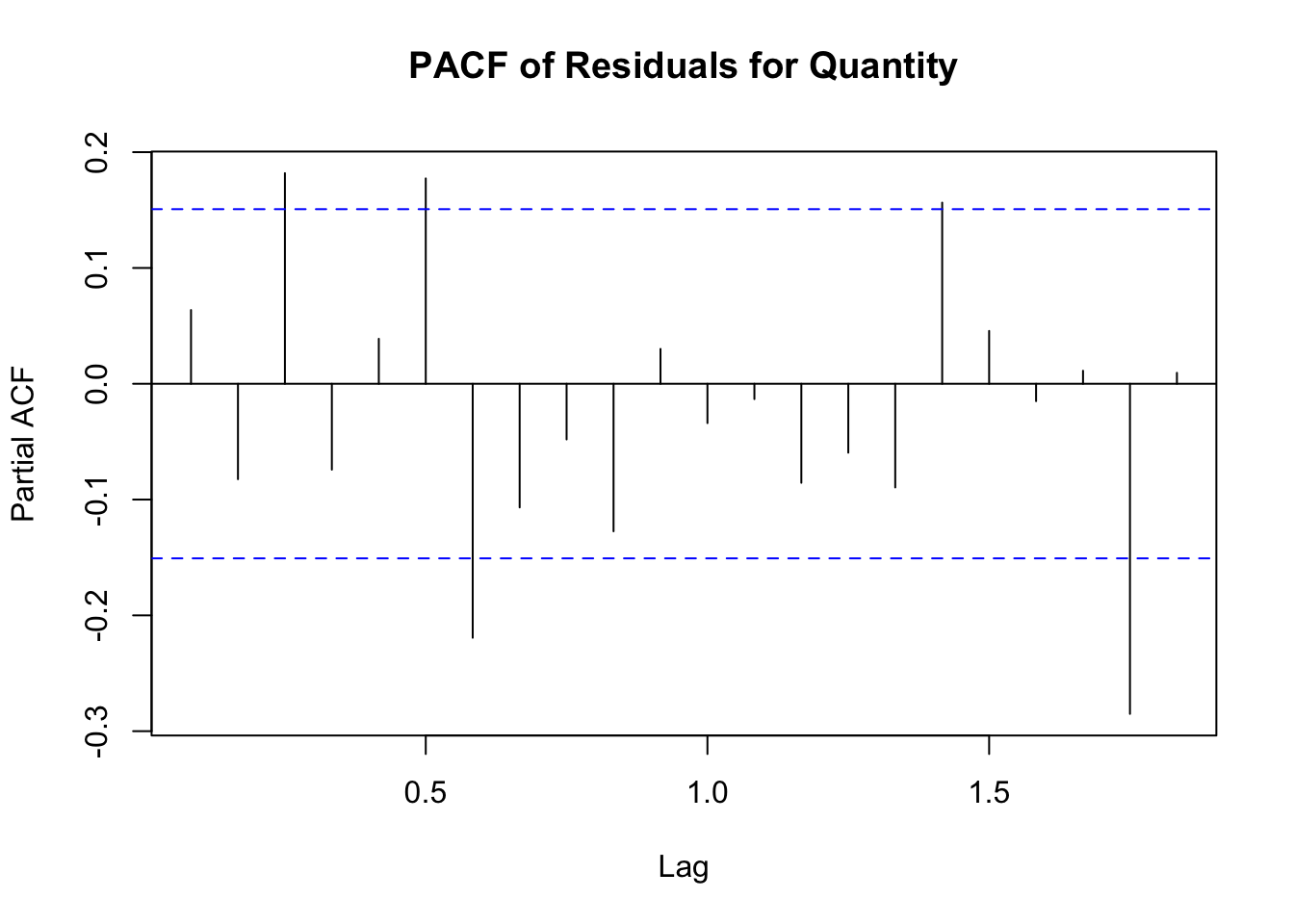

Residual Plot: Inspect the plot to ensure the residuals are centered around zero and exhibit constant variance. If there are patterns or trends in the residuals, it suggests that the model may need improvement.

Mean Squared Error (MSE): A smaller MSE indicates that the model’s predictions are closer to the actual values, implying better model performance.

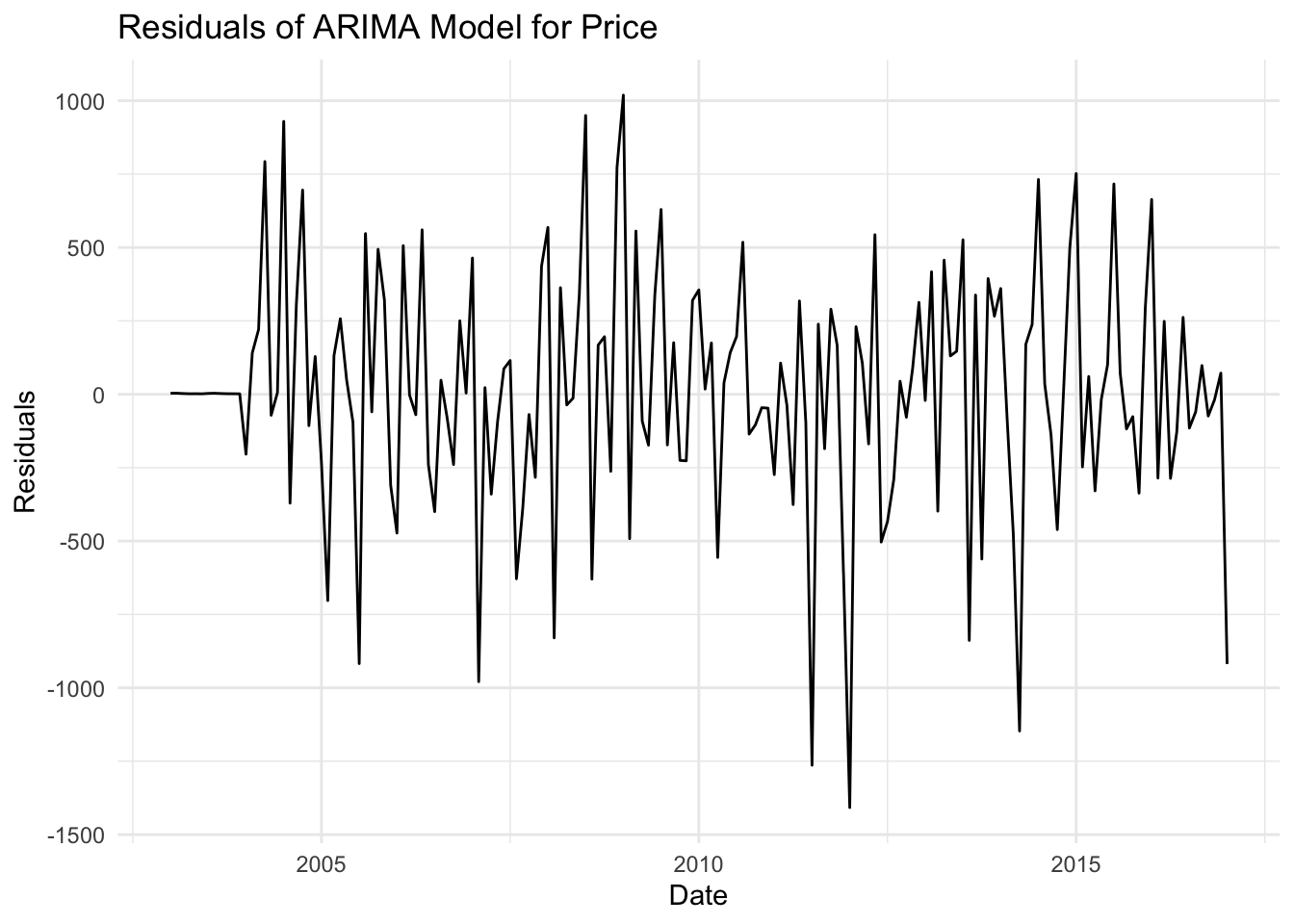

# Residualsresiduals_p <-residuals(fit_price)residuals_q <-residuals(fit_quan)# Plot residualsautoplot(residuals_p) +labs(title ="Price Residuals of ARIMA Model", x ="Date", y ="Residuals") +theme_minimal()

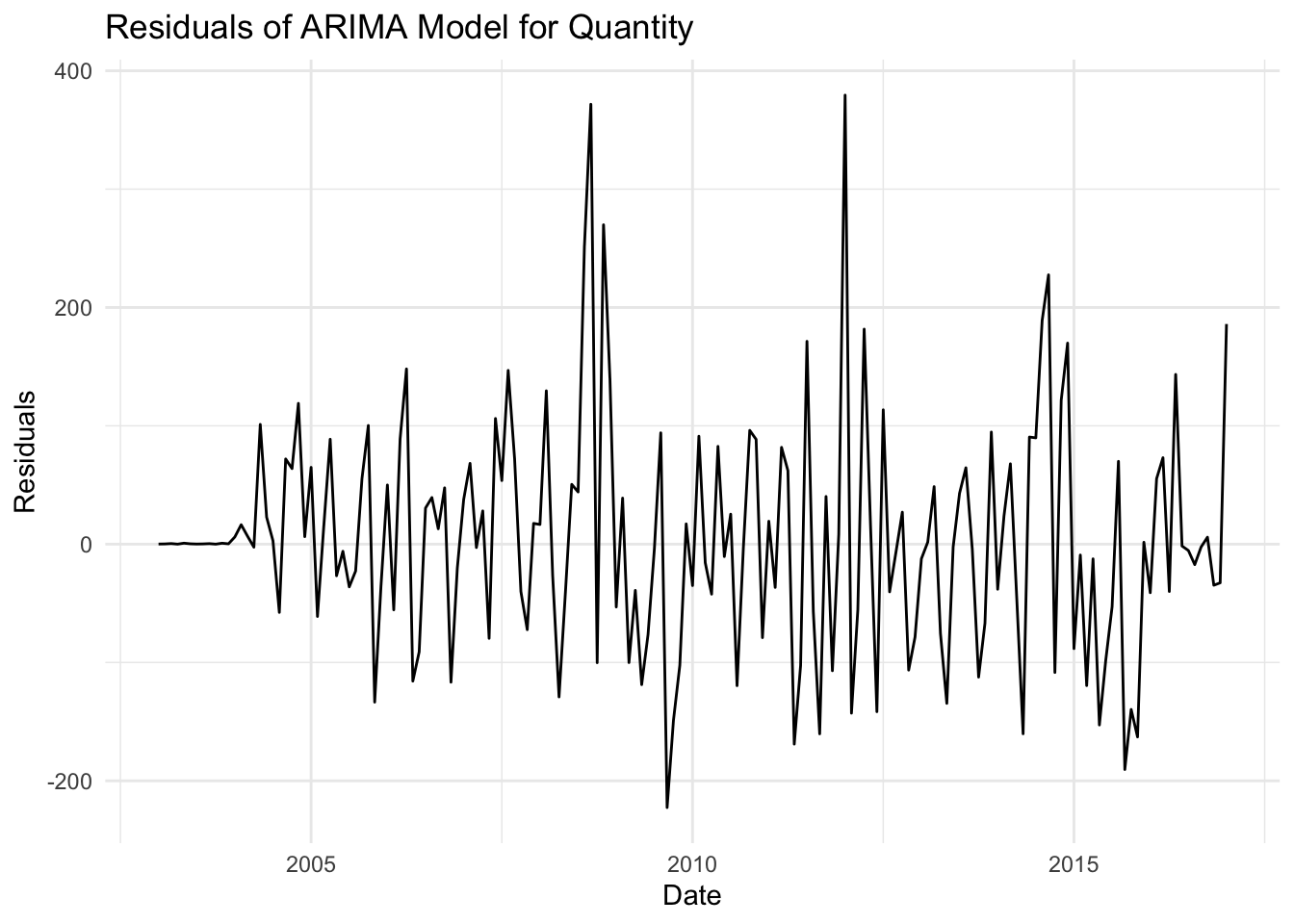

autoplot(residuals_q) +labs(title ="Quantity Residuals of ARIMA Model", x ="Date", y ="Residuals") +theme_minimal()

The price model shows moderate explanatory power (R² = 0.657), but the high MSE and RMSE indicate that the residuals are substantial, suggesting potential improvements or alternative modeling techniques might be needed.

Quantity Model:

The quantity model shows better performance with higher R² (0.775) and lower error metrics (MSE, RMSE, MAE), indicating a good fit and more accurate predictions compared to the price model.

7. Exploratory Data Analysis with Different Species

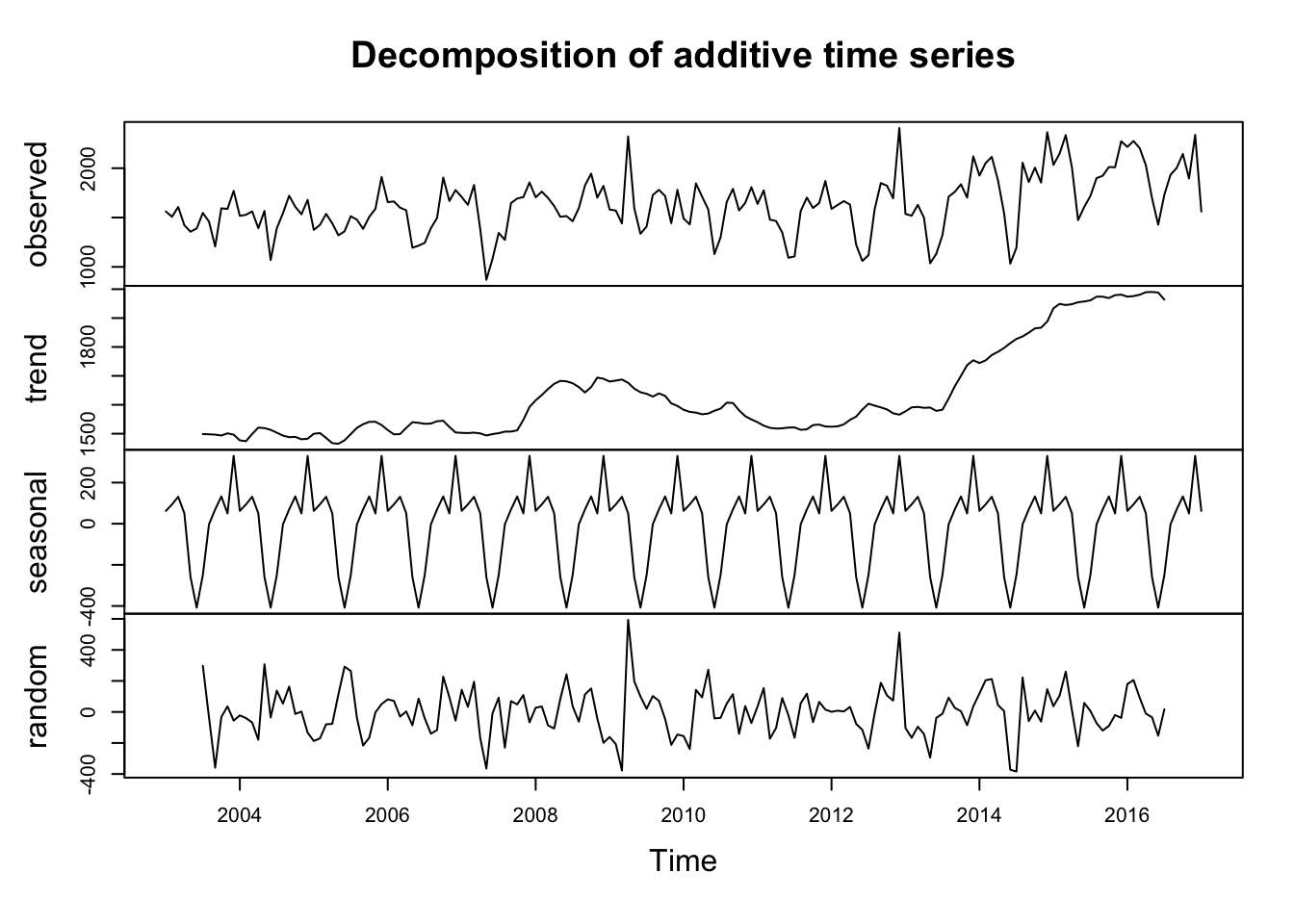

bt_price <- tuna %>%filter(measure =="Price", species =="Bluefin Tuna")ts_bt <-ts(bt_price$value, start =2003, end =2017, frequency =12) decomposed3 <-decompose(ts_bt)plot(decomposed3)

sbt_price <- tuna %>%filter(measure =="Price", species =="Southern Bluefin Tuna")ts_sbt <-ts(sbt_price$value, start =2003, end =2017, frequency =12) decomposed4 <-decompose(ts_sbt)plot(decomposed4)

bgt_price <- tuna %>%filter(measure =="Price", species =="Bigeye Tuna")ts_bgt <-ts(bgt_price$value, start =2003, end =2017, frequency =12) decomposed5 <-decompose(ts_bgt)plot(decomposed5)

Key Takeaways

Seasonal Component: Appears consistent, suggesting recurring patterns at regular intervals.

Trend Component: Bluefin Tuna has a predictable trend, however Southern Bluefin and Bigeye Tuna appears less predictable, both indicating potential long-term jump in price over time.

Random Component: Shows variability, indicating unexplained fluctuations or noise in the data.

# Quickly check for stationarityadf.test(ts_bt)

Warning in adf.test(ts_bt): p-value smaller than printed p-value

Augmented Dickey-Fuller Test

data: ts_bt

Dickey-Fuller = -4.0301, Lag order = 5, p-value = 0.01

alternative hypothesis: stationary

adf.test(ts_sbt)

Augmented Dickey-Fuller Test

data: ts_sbt

Dickey-Fuller = -1.5708, Lag order = 5, p-value = 0.7555

alternative hypothesis: stationary

adf.test(ts_bgt)

Warning in adf.test(ts_bgt): p-value smaller than printed p-value

Augmented Dickey-Fuller Test

data: ts_bgt

Dickey-Fuller = -6.438, Lag order = 5, p-value = 0.01

alternative hypothesis: stationary

Key Takeaways

Bluefin Tuna: Stationary

Southern Bluefin:Non-Stationary

Bigeye Tuna:Stationary

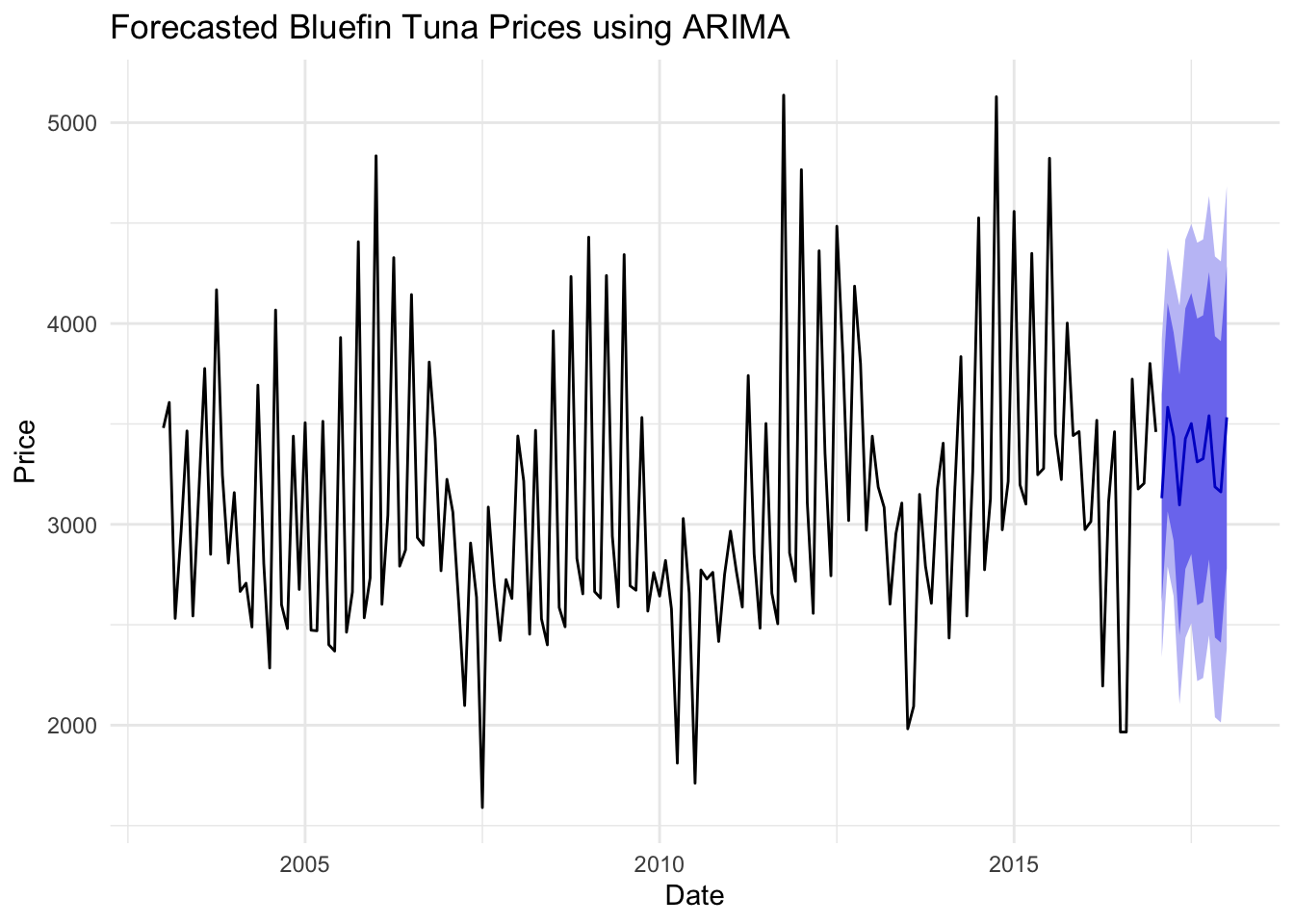

# Fit modelfit_bt <-auto.arima(ts_bt)fit_sbt <-auto.arima(ts_sbt)fit_bgt <-auto.arima(ts_bgt)summary(fit_bt)

Series: ts_bt

ARIMA(4,0,0)(2,0,1)[12] with non-zero mean

Coefficients:

ar1 ar2 ar3 ar4 sar1 sar2 sma1 mean

0.0691 -0.0463 0.7589 -0.1061 -0.7768 -0.3637 0.7588 3114.3466

s.e. 0.0788 0.0502 0.0496 0.0795 0.1202 0.0820 0.1127 75.9551

sigma^2 = 162826: log likelihood = -1254.42

AIC=2526.83 AICc=2527.96 BIC=2555

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set 2.517485 393.8503 296.0585 -1.518045 9.976024 0.4364676

ACF1

Training set 0.002743469

# Forecasting Different Specicesfore_price3 <-forecast(fit_bt, h =12) autoplot(fore_price3) +labs(title ="Forecasted Bluefin Tuna Prices using ARIMA", x ="Date", y ="Price") +theme_minimal()

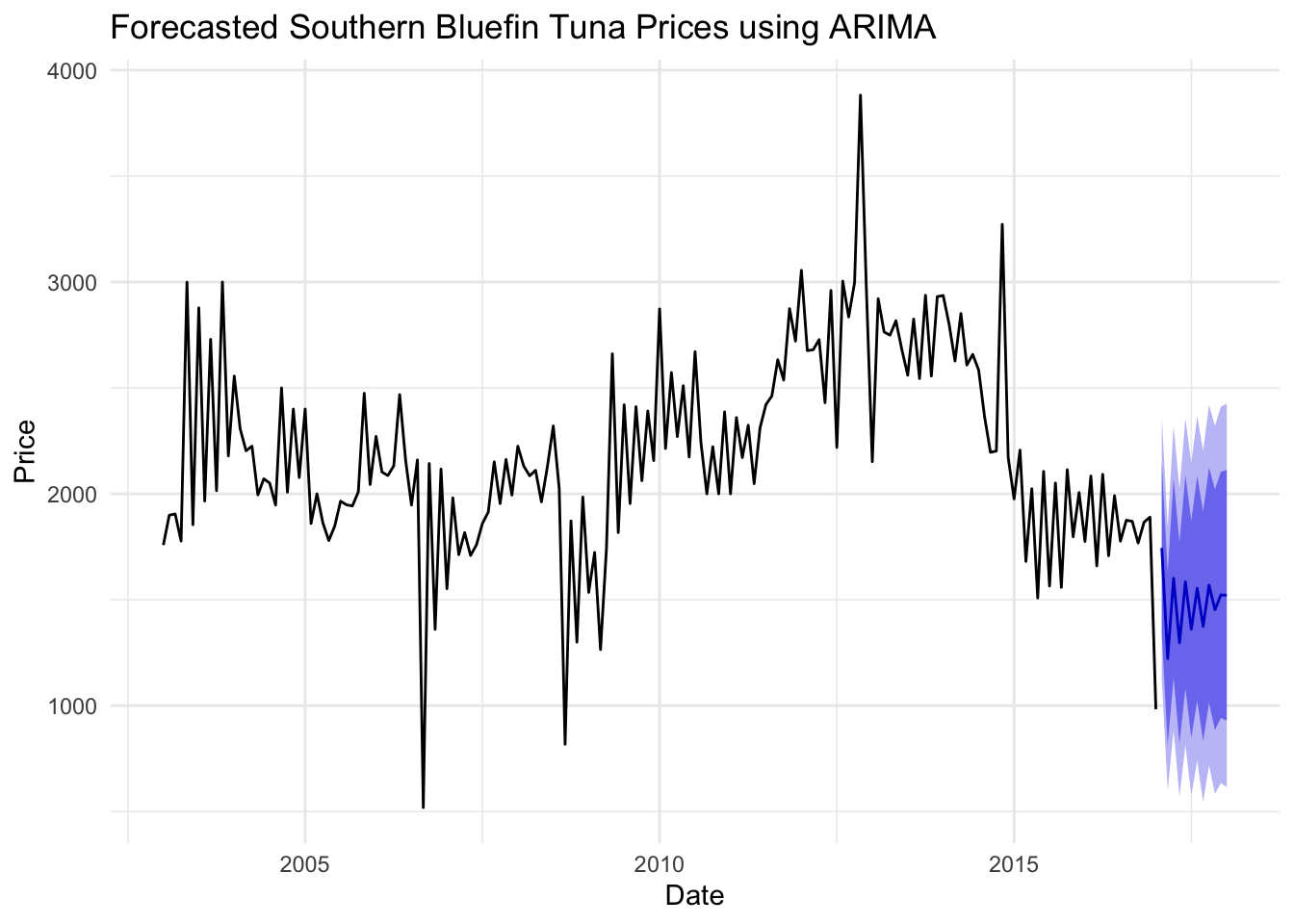

fore_price4 <-forecast(fit_sbt, h =12) autoplot(fore_price4) +labs(title ="Forecasted Southern Bluefin Tuna Prices using ARIMA", x ="Date", y ="Price") +theme_minimal()

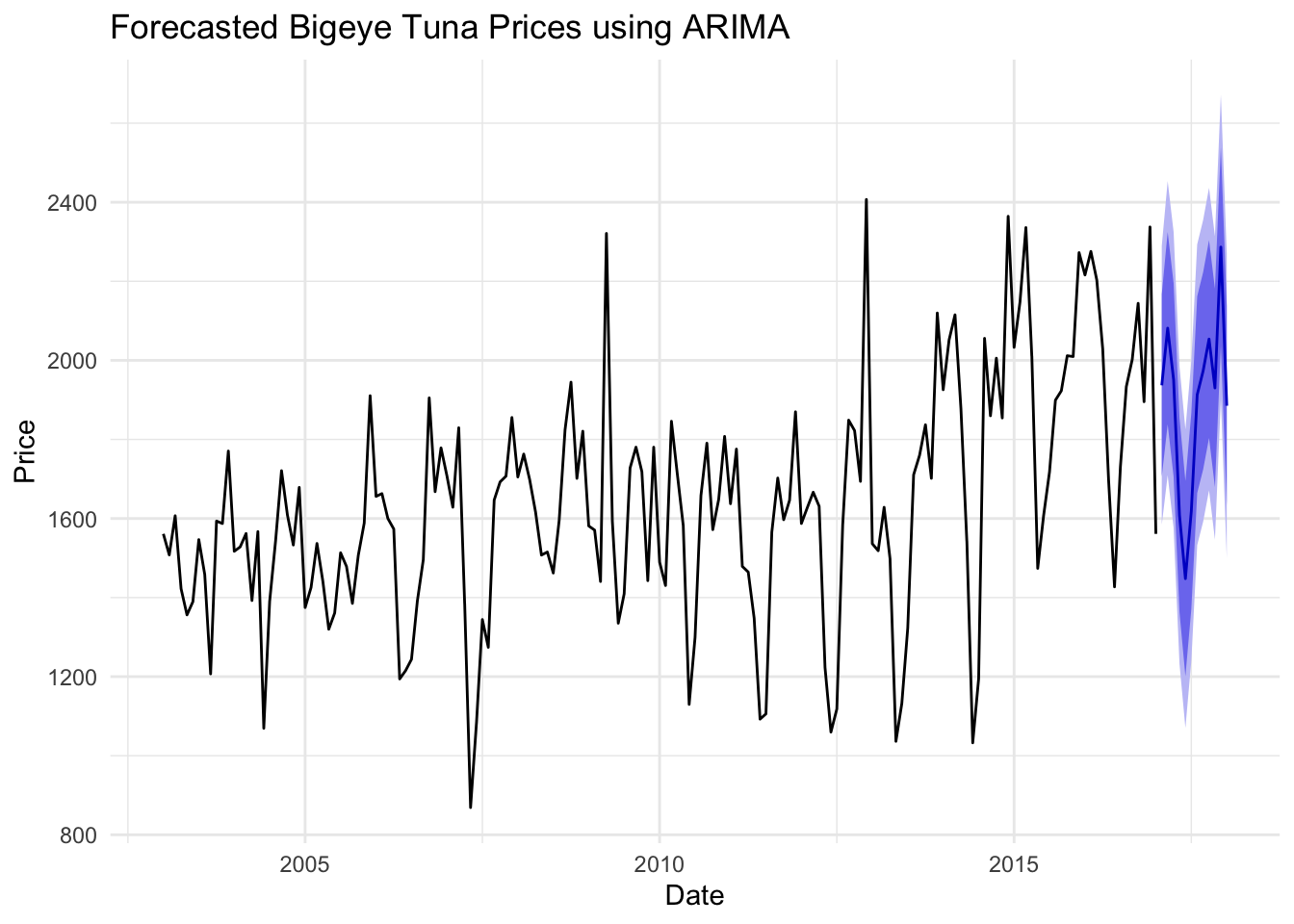

fore_price5 <-forecast(fit_bgt, h =12)autoplot(fore_price5) +labs(title ="Forecasted Bigeye Tuna Prices using ARIMA", x ="Date", y ="Price") +theme_minimal()

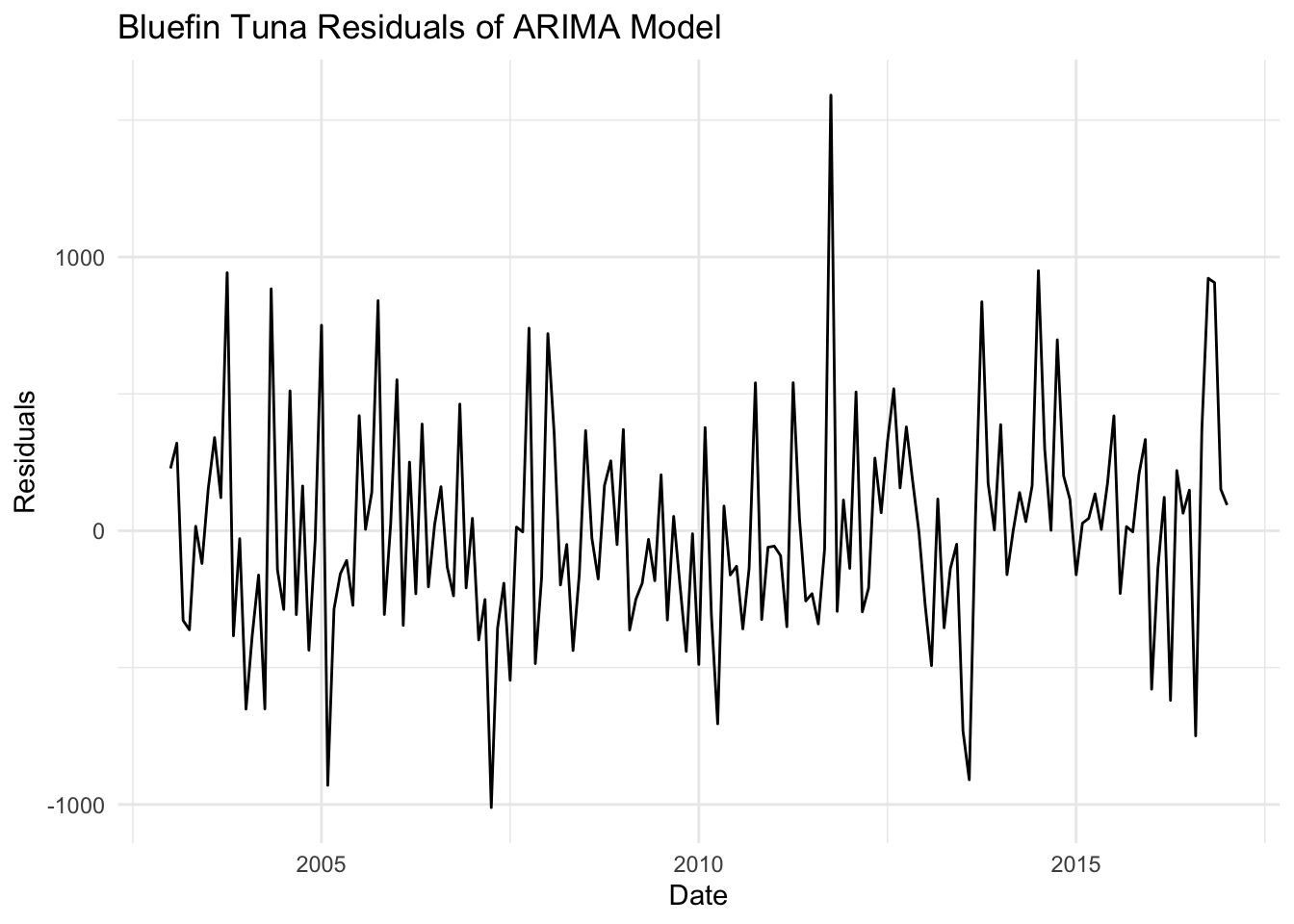

# Residualsresiduals_1 <-residuals(fit_bt)residuals_2 <-residuals(fit_sbt)residuals_3 <-residuals(fit_bgt)# Plot residualsautoplot(residuals_1) +labs(title ="Bluefin Tuna Residuals of ARIMA Model", x ="Date", y ="Residuals") +theme_minimal()

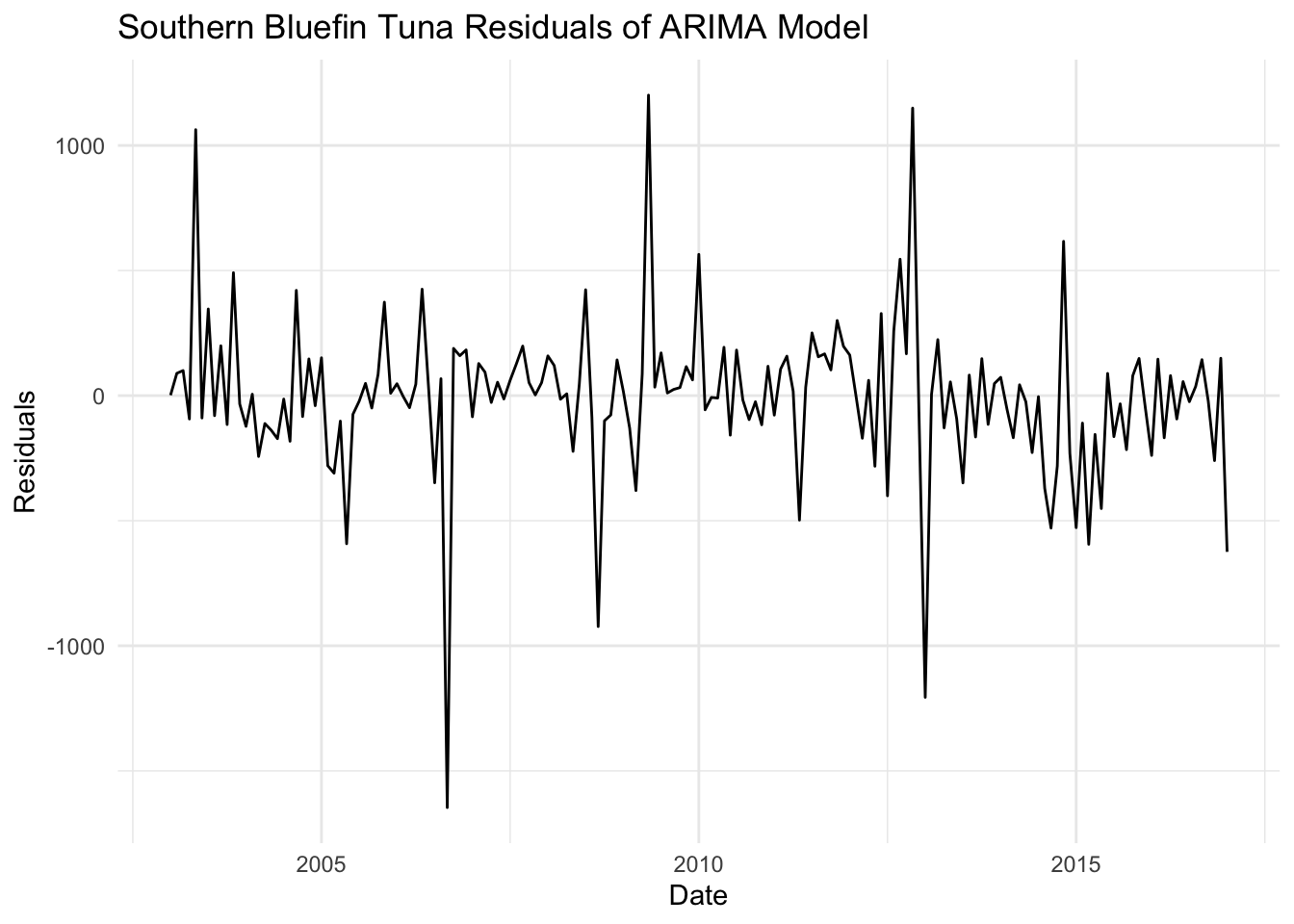

autoplot(residuals_2) +labs(title ="Southern Bluefin Tuna Residuals of ARIMA Model", x ="Date", y ="Residuals") +theme_minimal()

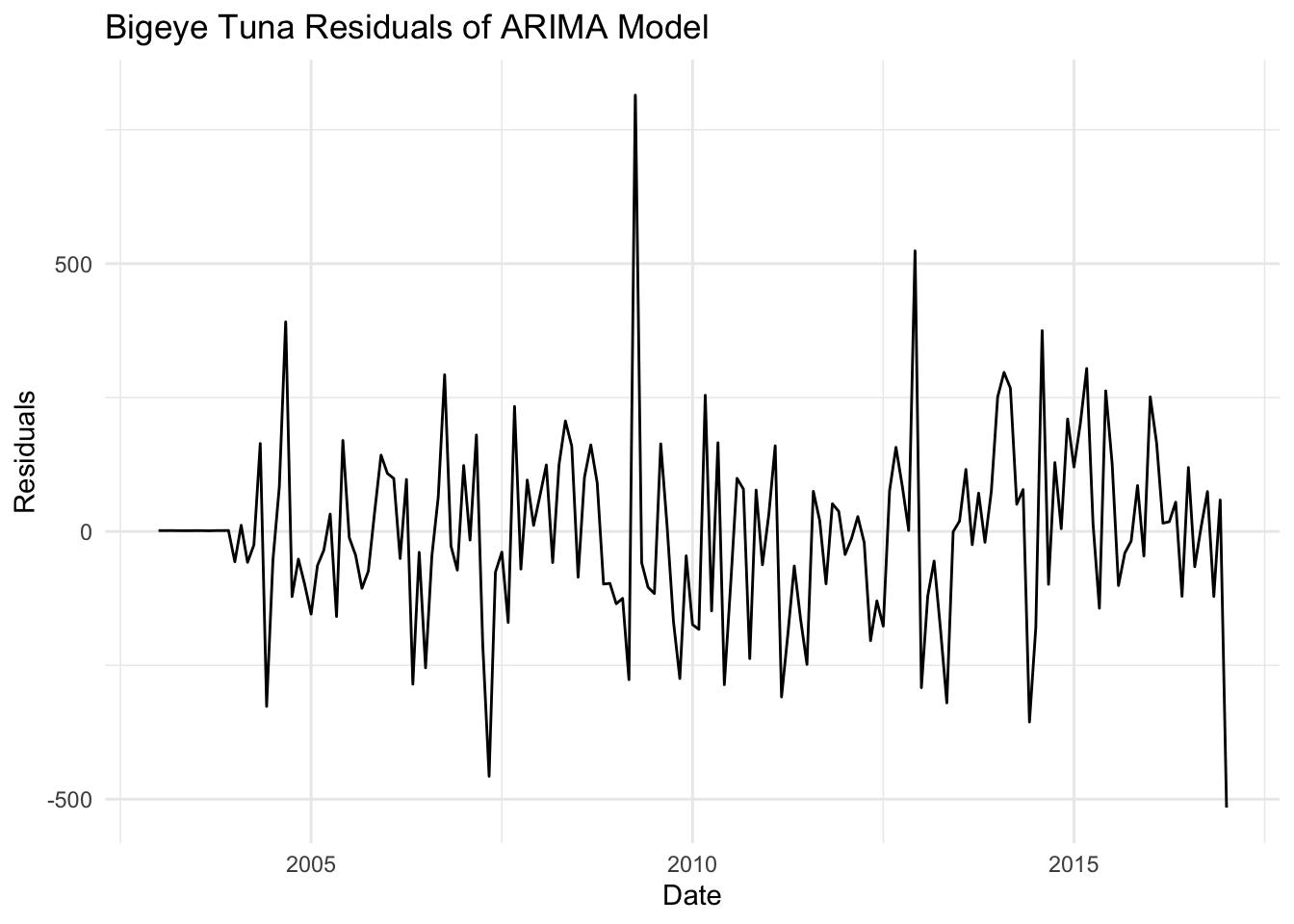

autoplot(residuals_3) +labs(title ="Bigeye Tuna Residuals of ARIMA Model", x ="Date", y ="Residuals") +theme_minimal()

In this analysis, I aimed to model and forecast tuna prices and quantities using ARIMA models. After refining the models, there were significant improvements in the performance metrics for both the price and quantity models.

The updated price model shows a substantial reduction in error metrics and an increase in explanatory power, with the R-squared value improving from 0.657 to 0.737. This indicates that the model now explains approximately 73.72% of the variance in the price data, suggesting a more accurate and reliable model.

The quantity model also shows improved performance, with lower error metrics and a higher R-squared value, now at 0.86291. This indicates that the model explains about 86.29% of the variance in the quantity data.

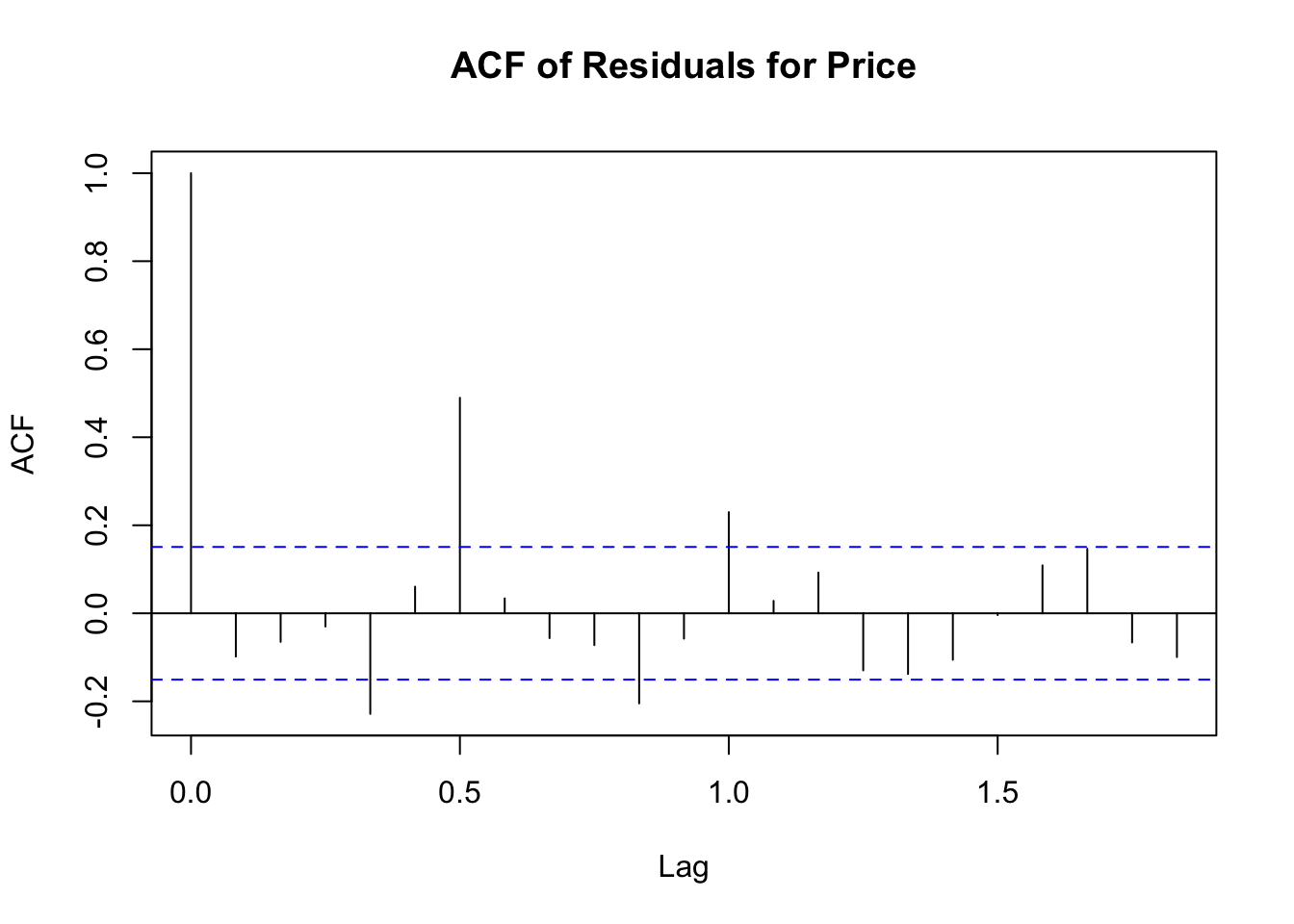

The p-values for both tests are significantly lower than 0.05, indicating that there is still some autocorrelation in the residuals, suggesting that the models could be further refined. However, the current models still provide a substantial improvement over the initial attempts.